Purchasing a home is one of the biggest financial decisions most people will make, and one of the first steps in the process is figuring out your down payment options. Whether you are a first-time homebuyer or looking to upgrade, understanding how much down payment you need and the various options available can make the difference between securing your dream home or facing delays. Different types of loans, such as FHA and conventional loans, offer varying down payment requirements, making it important to explore all avenues to find the best fit for your financial situation.

In this guide, we will break down the most common down payment options, explain how they affect your mortgage approval, and provide tips on how you can lower your upfront costs. From low down payment programs to down payment assistance, we’ll help you navigate the complexities of buying a home with ease.

What Are Down Payment Options for Homebuyers in 2024?

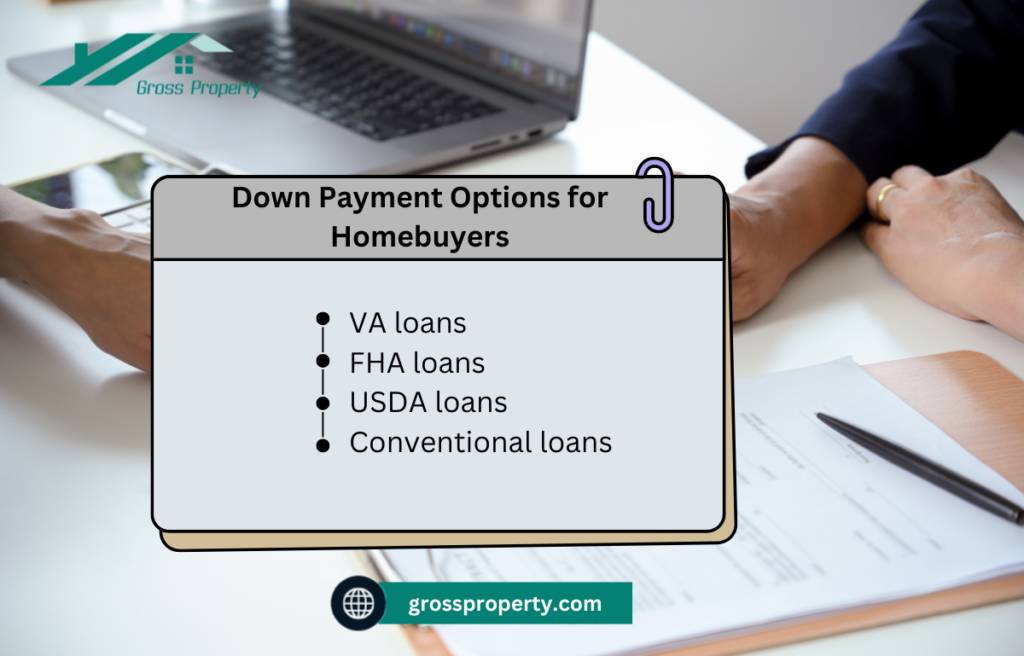

In 2024, homebuyers have a range of down payment options that cater to different financial situations, making homeownership more accessible than ever. The most common options are conventional loans, FHA loans, VA loans, and USDA loans. Conventional loans typically require a down payment of 5-20%, while FHA loans are designed for low-to-moderate-income buyers, allowing down payments as low as 3.5%. VA loans, available to military veterans, often require no down payment, and USDA loans, which are aimed at rural homebuyers, also offer zero-down options.

Additionally, there are numerous down payment assistance programs in place that offer grants or low-interest loans to help cover part of the down payment. These programs are often targeted at first-time homebuyers and low-income individuals. In 2024, many states and local governments are expanding these programs to increase homeownership opportunities. Therefore, understanding and exploring these options is crucial for prospective buyers.

Saving for a down payment remains a major hurdle for many buyers, but 2024’s flexible down payment options and assistance programs are designed to reduce this barrier. Buyers should evaluate their eligibility for these programs and choose the option that aligns best with their financial capabilities and long-term plans.

How Do Down Payment Options Differ Between FHA and Conventional Loans?

FHA loans and conventional loans differ significantly when it comes to down payment options. FHA loans, backed by the Federal Housing Administration, are designed to make homeownership accessible to a broader range of buyers, particularly those with lower credit scores or limited savings. The minimum down payment for an FHA loan is 3.5%, making it one of the most popular choices for first-time homebuyers or buyers with less cash on hand.

In contrast, conventional loans are not government-backed and typically require a higher down payment, usually starting at 5%. However, some conventional loan programs, such as Fannie Mae’s HomeReady or Freddie Mac’s Home Possible, offer down payments as low as 3% for qualified buyers. One of the major advantages of conventional loans is that buyers who put down 20% or more can avoid private mortgage insurance (PMI), whereas FHA loans require mortgage insurance regardless of the down payment amount.

Additionally, FHA loans have more flexible qualification standards, allowing for lower credit scores and higher debt-to-income ratios, whereas conventional loans typically have stricter credit and income requirements. Buyers should carefully assess both options based on their financial situation and long-term goals.

How Much Down Payment Is Needed to Buy a House?

The amount of down payment needed to buy a house in 2024 depends largely on the type of mortgage loan you choose and your financial situation. For a conventional mortgage, most lenders require a minimum down payment of 5%, though putting down 20% is often recommended to avoid private mortgage insurance (PMI). On the other hand, government-backed loans such as FHA loans only require 3.5%, making homeownership more accessible for those with lower savings.

The other down payment options include zero-down payment loans available, such as VA loans for veterans and USDA loans for eligible rural buyers. While no down payment sounds attractive, it often leads to higher monthly mortgage payments and, in some cases, stricter lending requirements. Each of these options has its trade-offs, and buyers need to assess their own financial goals to determine how much they should put down.

Generally, a larger down payment reduces the overall mortgage size, potentially lowering monthly payments and interest costs over the loan’s life. Homebuyers in 2024 should carefully assess their down payment options and choose the one that aligns with their long-term financial goals.

What Are the Benefits of Making a Larger Down Payment?

Making a larger down payment when buying a home in 2024 can offer several significant benefits. First, a larger down payment reduces the size of your mortgage, which in turn reduces your monthly payments and the amount of interest you will pay over the life of the loan. This makes homeownership more affordable in the long run, as less money is spent on interest.

Another key benefit is the ability to avoid private mortgage insurance (PMI), which is typically required when borrowers put down less than 20% on a home purchase. PMI can add hundreds of dollars to your monthly mortgage payment, so avoiding it by making a larger down payment can result in substantial savings. Additionally, buyers who can put down more upfront may also have access to better mortgage rates, as lenders often view these buyers as lower risk.

Finally, making a larger down payment increases your home equity right from the start, providing more financial security. If property values decline, having more equity can protect you from owing more on your mortgage than your home is worth. Thus, while saving for a larger down payment might take more time, the long-term financial advantages make it an appealing option for many buyers.

How Does a Low Down Payment Affect Mortgage Approval?

Opting for low down payment options can make it easier to buy a home, but it may also affect the mortgage approval process. Lenders view a smaller down payment as a higher risk because it provides less upfront equity. As a result, buyers with low down payments may face stricter qualification criteria, including higher credit score requirements and more extensive income verification. In some cases, lenders might charge higher interest rates to offset the increased risk.

One of the biggest impacts of a low down payment is the requirement for private mortgage insurance (PMI). If you put down less than 20% on a conventional loan, lenders typically require PMI, which increases your monthly mortgage payment. PMI protects the lender in case you default on the loan, but it adds an extra financial burden to homebuyers.

However, low down payment options, such as FHA loans or VA loans, can still make homeownership achievable for many. While you might pay more in the long run due to PMI or higher interest rates, these loans provide an opportunity for individuals without significant savings to enter the housing market. Buyers should weigh the pros and cons of a low down payment based on their financial goals and long-term affordability.

How Does a Down Payment Affect Monthly Mortgage Payments?

The size of your down payment has a direct impact on your monthly mortgage payments. When you make a larger down payment, you are borrowing less money from the lender, which results in lower monthly payments. This is because the total amount of interest you will pay over the life of the loan decreases when the loan principal is smaller. For example, a 20% down payment on a $300,000 home would leave you with a $240,000 loan, whereas a 5% down payment would result in a $285,000 loan. Even though both options allow you to buy the home, the smaller loan leads to more affordable monthly payments.

Additionally, with a larger down payment options, you can often avoid paying for private mortgage insurance (PMI). PMI is typically required on conventional loans when you put down less than 20%, and it increases your monthly payment. By putting down 20% or more, you eliminate the need for PMI, resulting in lower overall housing costs.

On the other hand, a smaller down payment might help you buy a house sooner, but it will lead to higher monthly payments. This option may work for buyers with limited savings but higher incomes, who can handle the larger monthly mortgage costs. Therefore, it’s important to weigh the benefits of a larger down payment against your immediate cash flow needs.

What Down Payment Options Are Available for First-Time Homebuyers?

First-time homebuyers in 2024 have several down payment options that make purchasing a home more achievable, even with limited savings. FHA loans are one of the most popular options for first-time buyers, requiring only a 3.5% down payment. This government-backed loan allows individuals with lower credit scores and smaller savings to qualify for home financing. Additionally, many lenders offer conventional loans with down payments as low as 3% through programs like Fannie Mae’s HomeReady and Freddie Mac’s Home Possible.

Apart from these loans, first-time homebuyers can also explore down payment assistance programs, which are often provided by state and local governments. These programs offer grants or low-interest loans to cover a portion of the down payment. Some programs are designed specifically for low- and moderate-income buyers, helping to further reduce upfront costs. For example, the Good Neighbor Next Door Program offers substantial discounts for public service professionals, including teachers and firefighters, making home ownership more affordable.

Given these various options, first-time buyers in 2024 can choose a plan that best fits their financial situation. Understanding the eligibility requirements and benefits of each program is essential in finding the right solution for your down payment needs.

What Are the Best Government Programs for Low Down Payments?

Several government programs in 2024 offer low down payment options, making homeownership more accessible for buyers who might struggle to save for a traditional 20% down payment. The FHA loan program is among the most widely used, allowing down payments as low as 3.5%. This program is ideal for buyers with lower credit scores or limited savings and offers competitive interest rates.

Another excellent option is the VA loan, available to military service members, veterans, and their families. VA loans often require no down payment and do not require private mortgage insurance (PMI), making them one of the best deals available for eligible buyers. Similarly, the USDA loan program offers zero-down payment options for buyers in rural areas, as long as they meet specific income and location requirements.

In addition to these federal programs, many states and local governments offer down payment assistance programs, including grants and low-interest loans, to cover down payment and closing costs. These programs, often aimed at first-time homebuyers and low-income households, can significantly reduce the upfront costs of purchasing a home. Buyers should explore all available resources to determine which government-backed program best meets their needs.

What Are the Pros and Cons of Down Payment Assistance Programs?

Down payment assistance programs are a valuable resource for homebuyers in 2024, but like any financial product, they come with both pros and cons. One of the primary advantages is that these programs can help reduce the upfront costs of purchasing a home, making homeownership more accessible, particularly for first-time and low-income buyers. Many programs offer grants, forgivable loans, or low-interest loans to cover a portion of the down payment, easing the financial burden.

Another benefit is that these programs can sometimes be combined with other government-backed loans, such as FHA loans, to further reduce costs. This can be especially useful for buyers who may not qualify for conventional loans due to credit or income limitations. Down payment assistance programs may also offer educational resources to help new homeowners navigate the buying process.

On the downside, many down payment assistance programs come with strict eligibility requirements, such as income limits or first-time homebuyer status. Some programs also have repayment terms that must be met, such as remaining in the home for a certain number of years, or the loan may need to be repaid in full. Additionally, homes purchased using these programs may be subject to price caps, which could limit the buyer’s options.

Can You Buy a House With No Down Payment?

Yes, you can buy a house with no down payment through specific mortgage programs in 2024. The two primary options are VA loans and USDA loans, both of which offer no down payment requirements, making homeownership more accessible to specific groups of buyers. VA loans are designed for military service members, veterans, and their families, allowing them to finance 100% of the home’s purchase price without requiring any money upfront. Additionally, these loans do not require private mortgage insurance (PMI), saving buyers significant costs over the life of the loan.

USDA loans offer another zero-down payment option for buyers purchasing homes in designated rural and suburban areas. These loans, backed by the U.S. Department of Agriculture, cater to low- to moderate-income buyers who meet location and income eligibility requirements. Like VA loans, USDA loans also have no PMI requirement, although there are additional income and location restrictions to qualify for this type of loan.

While these no down payment options can be attractive, they do come with certain trade-offs. Buyers may face higher monthly mortgage payments due to financing the entire purchase price, and interest rates may be slightly higher to offset the risk for lenders. However, for buyers with limited savings, these options provide a clear path to homeownership.

What Are Creative Down Payment Solutions for Buyers With Limited Funds?

For buyers with limited funds, finding creative down payment solutions can make the difference between homeownership and waiting for years to save. One common option is to use down payment assistance programs, which provide grants or low-interest loans to help cover the initial costs. These programs, often offered by state or local governments, can significantly reduce the amount of money you need to save. Some programs are specifically designed for first-time homebuyers or low-income buyers, making them an excellent option for those with limited resources.

Another creative solution is using gifts from family members. Lenders often allow buyers to receive down payment gifts from relatives, as long as the funds are properly documented and verified. This can be a great way to bridge the gap between your savings and the down payment requirement. In addition, some buyers choose to liquidate other assets, such as selling stocks or using retirement savings (with careful consideration of tax penalties and future financial impact).

Finally, some lenders offer down payment installment plans or lease-to-own agreements, where a portion of your rent goes toward the eventual down payment. These alternative paths provide more flexibility for buyers who need time to save but want to move into their homes sooner.

What Is the Difference Between a Down Payment and Closing Costs?

The down payment and closing costs are two separate financial components involved in purchasing a home, and it’s important to understand the distinction between them. The down payment is a percentage of the home’s purchase price that the buyer pays upfront. This payment reduces the loan amount, effectively acting as a commitment to the lender that you are financially invested in the property. Most lenders require a minimum down payment ranging from 3% to 20%, depending on the type of loan and borrower qualifications.

In contrast, closing costs are the fees associated with the process of buying a home. These fees typically include loan origination charges, title insurance, appraisal fees, legal fees, and escrow deposits, among others. Closing costs usually range from 2% to 5% of the home’s purchase price and are paid at the time of closing, in addition to the down payment. While some closing costs can be negotiated or covered by the seller, buyers should budget for these expenses separately from the down payment.

Both the down payment and closing costs are crucial to homeownership, but they serve different purposes in the home-buying process. It’s essential to plan for both when calculating the total cost of purchasing a home.

Navigating the world of down payment options is a crucial step in the home-buying process. Whether you’re a first-time buyer exploring low down payment programs or an experienced homeowner looking to make a larger investment, understanding the impact of your down payment choice is essential for long-term financial stability. A larger down payment not only reduces your monthly mortgage payments but also saves you from the burden of private mortgage insurance (PMI), making homeownership more affordable in the long run.

For those with limited funds, there are several creative down payment solutions available, from government-backed assistance programs to gifts from family members and lease-to-own options. These alternatives can help buyers bridge the financial gap and enter the housing market sooner without compromising their future financial health.

Finally, while the down payment is a major part of purchasing a home, buyers must also budget for closing costs, which can add an additional 2-5% to the total expense. Planning for both upfront costs ensures a smoother home-buying process and sets the stage for a more secure financial future in homeownership. By understanding and evaluating all available down payment options, buyers can make informed decisions that align with their financial goals.